State of Physical AI 2026: The robots are coming, but not the way you think

The sector is real. The volume and the margin accrue to China. The only defensible long is a narrow set of chokepoints bought on weakness, not the basket everyone is loading.

The consensus on physical AI is that it is the next multi-trillion-dollar trade and that you are early. Jensen Huang has put a $40 trillion total addressable market on robotics and “physical AI” from the GTC stage, the humanoid OEM names have run 40 to 150 percent off the theme, Korean robotics is up 40 to 53 percent year-to-date, and the AI-robotics token basket has rallied on the same narrative. The frame is that a new category is being born and the entire value chain re-rates together.

That frame is half right, and the half that is wrong is the half you are being asked to pay for. Physical AI is real as a destination. It is not real as a 2026 basket. The actual shipment floor this year is measured in low tens of thousands of units globally, not millions. The unit economics of the flagship products are collapsing under a deliberate Chinese price attack, not expanding. The layer of the bill of materials where value actually accrues is being commoditized by the same Chinese supply chain that already won drones and batteries. And the “revenue” inside the on-chain robotics basket is, on a verified basis, almost entirely subsidy-masked or simulated.

My governing view: the post-Jensen physical AI basket is mispriced exit liquidity. The sector is real, but the volume and the margin accrue to China, so the only defensible long is a narrow set of chokepoints and data-moats bought on weakness, not the basket. This essay builds that case from the shipment data up, names what I would own and what I would avoid, and is honest about the two places where my own thesis is underbuilt.

I. The $40 trillion number is a destination, not a 2026 entry: the global humanoid installed base is roughly 16,000 to 18,000 units

Start with the number that matters and almost nobody quotes: how many humanoid robots actually exist and do work today. Per cross-referenced 2025 disclosures and SemiAnalysis fieldwork, the global installed base of humanoid robots at the end of 2025 is approximately 16,000 to 18,000 units, and the overwhelming majority of those are non-full-size research and education platforms, not industrial labor. The headline that the market is “inflecting” to 50,000 to 100,000 units in 2026 is true only with three asterisks: it is a China story, a low-spec story, and a target story, not a global, full-size, shipped-and-deployed story.

Walk the actuals, because the actuals are the whole argument.

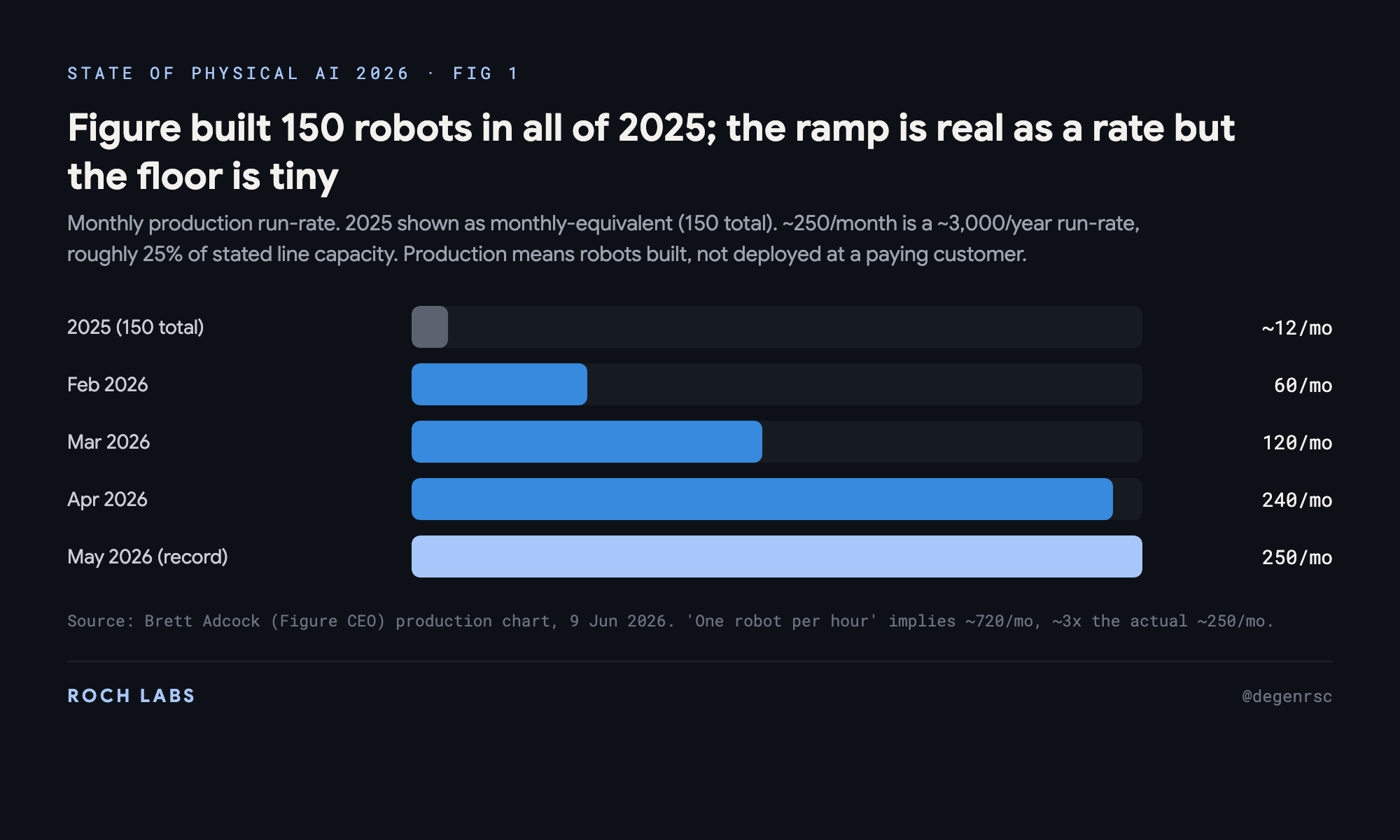

Figure, the US foundation-model-plus-hardware darling, built 150 robots in all of 2025. Per the company’s own CEO chart published in June 2026, Figure reached roughly 250 units per month by May 2026. That is a real ramp as a rate, and it is a roughly 3,000-per-year run-rate that is approximately 25 percent of the company’s stated 12,000-per-year BotQ line capacity. The “one robot per hour” headline that circulated implies roughly 720 per month, which is about three times the actual ~250. And every one of these is a production unit, a robot built, not a deployed-at-customer revenue unit. The gap between “built” and “doing paid work” is the entire commercial question, and it is wide.

Unitree, the Chinese cost leader, shipped approximately 5,500 units in 2025. Per SemiAnalysis, roughly 70 percent of those were non-full-size research and education units, and only on the order of 250 were in actual labor settings. Unitree’s 2026 target is 20,000 units. UBTech, the Hong-Kong-listed industrial humanoid name, shipped 1,079 full-size industrial units in 2025 at a 54.6 percent gross margin, targets roughly 5,000 in 2026 and 10,000 by 2027. Tesla’s Optimus shipped “hundreds” in 2025, all internal and for learning, against a 50,000 to 100,000 target for 2026 that realistically maps to “low thousands” of genuinely deployed units.

Now stack the targets against the prior-year actuals: Unitree is guiding 20,000 after 5,500, UBTech roughly 5,000 after 1,079, Tesla 50,000 to 100,000 after “hundreds.” These are 3x to 4x year-over-year ramps quoted as fact. The trade is not wrong that shipments are growing. It is wrong about where they are growing and how small the floor actually is. China’s domestic humanoid installed base went from roughly 18,000 in 2025 toward a 62,500 target for 2026 per state media, and that single national number is essentially the entire “global” 50,000 to 100,000 range that gets quoted as a worldwide inflection. The inflection is China plus low-spec plus targets. Own that sentence before you own the basket.

The honest counterpoint here: a 3,000-per-year run-rate at Figure and a 20,000 target at Unitree are still exponential against a base of zero, and exponentials are exactly what you want to be early to. I agree. The disagreement is not about direction. It is about what you are paying for that direction, and to whom the economics of it accrue, which is the rest of this essay.

II. The robot is a mechatronics problem, not a chip problem: actuation is 40 to 66 percent of the bill of materials and compute is 8 percent, falling to 5

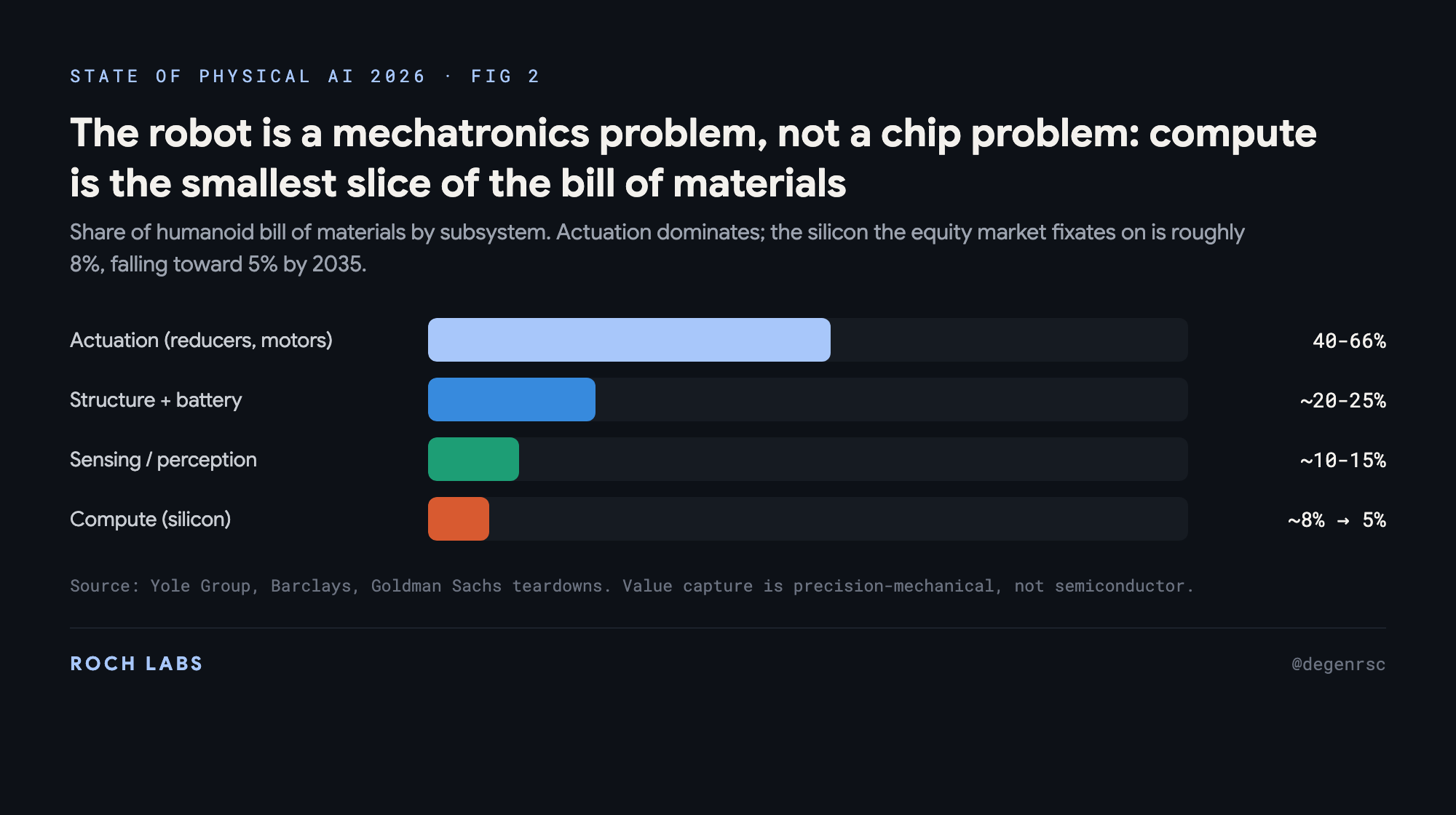

The instinct that has worked for three years is “buy the picks and shovels, buy NVIDIA.” Applied to humanoids, that instinct buys the wrong tier of the chain. Per Yole Group, the silicon content of a humanoid robot is approximately 8 percent of the bill of materials today and is expected to fall toward 5 percent by 2035 as compute commoditizes and the rest of the body does not. The dominant cost is actuation: the reducers, motors, and screws that let the robot move are 40 to 66 percent of the bill of materials per Yole, Barclays, and Goldman teardowns. Structure and battery are roughly 20 to 25 percent. Sensing and perception are roughly 10 to 15 percent. Compute, the part the equity market fixates on, is the smallest slice.

This is not a footnote. It is the single most important reframe in the sector, because it tells you that the durable value-capture in humanoids is a precision-mechanical problem, not a semiconductor problem, and precision mechanics is a domain where the Western incumbents are being actively undercut rather than one where they have a widening moat.

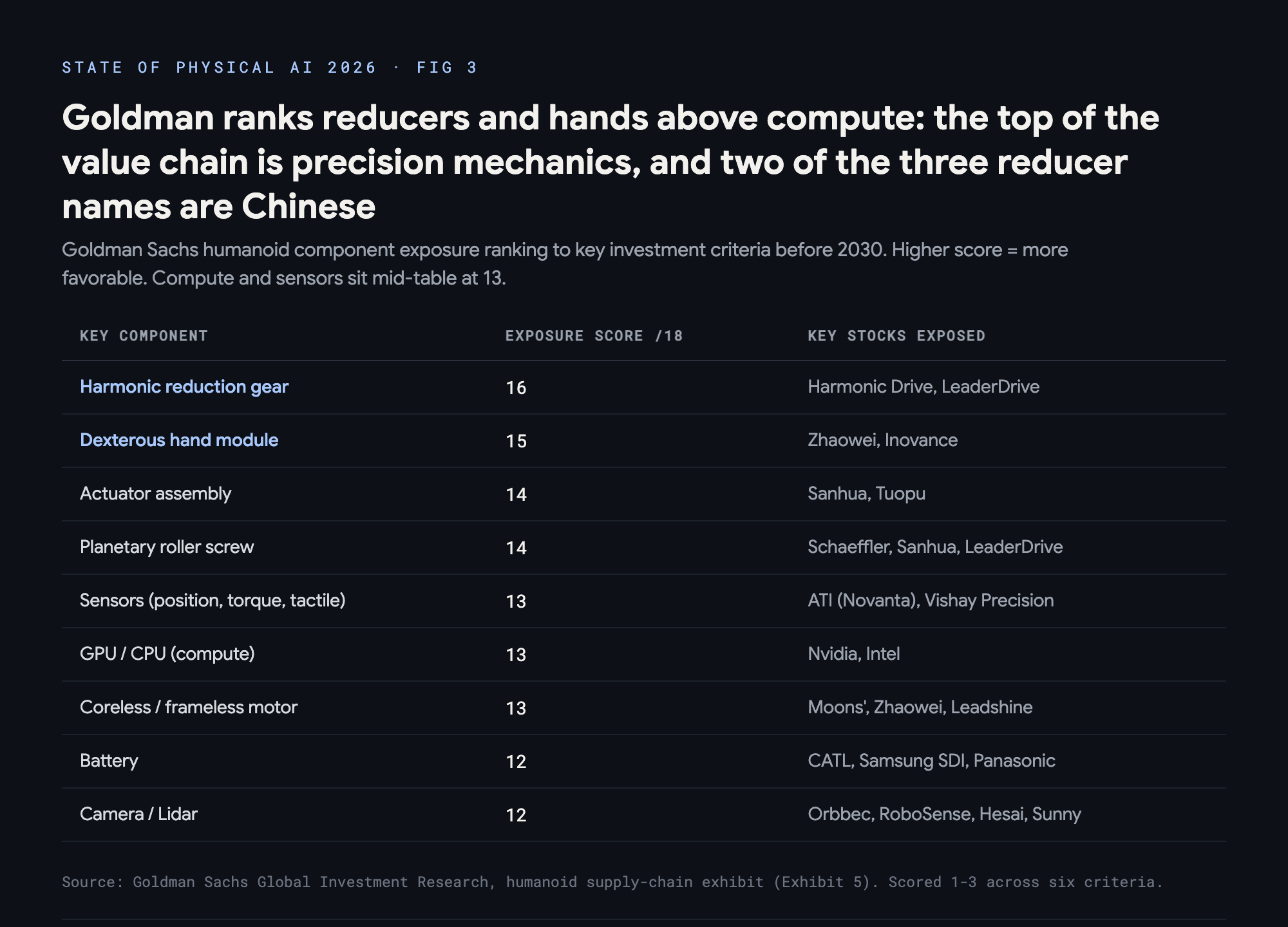

Goldman’s own component-exposure work makes the point in their preferred language. In Goldman’s humanoid supply-chain exhibit, the components ranked highest on combined investment criteria before 2030 are harmonic reduction gears, scored 16 out of a possible 18, followed by dexterous hand modules at 15, then actuator assembly and planetary roller screws at 14, then sensors and compute tied at 13, then battery and camera at 12. Compute and sensors sit in the middle of Goldman’s own hierarchy, not the top. The top is reducers and hands. The names Goldman attaches to the reducer line are Harmonic Drive and LeaderDrive. The names attached to the hand line are Chinese: Zhaowei, Inovance.

If you accept Goldman’s hierarchy, and the hardware physics says you should, then the question for the long side is simple: who owns the reducer and the actuator, and is their margin expanding or contracting as volume scales? The answer is uncomfortable, and it is the next two sections.

III. China is running the BYD and DJI playbook on the hardest component: Unitree’s flagship fell from $50,000 to $27,300 in roughly 18 months at a 67 percent gross margin

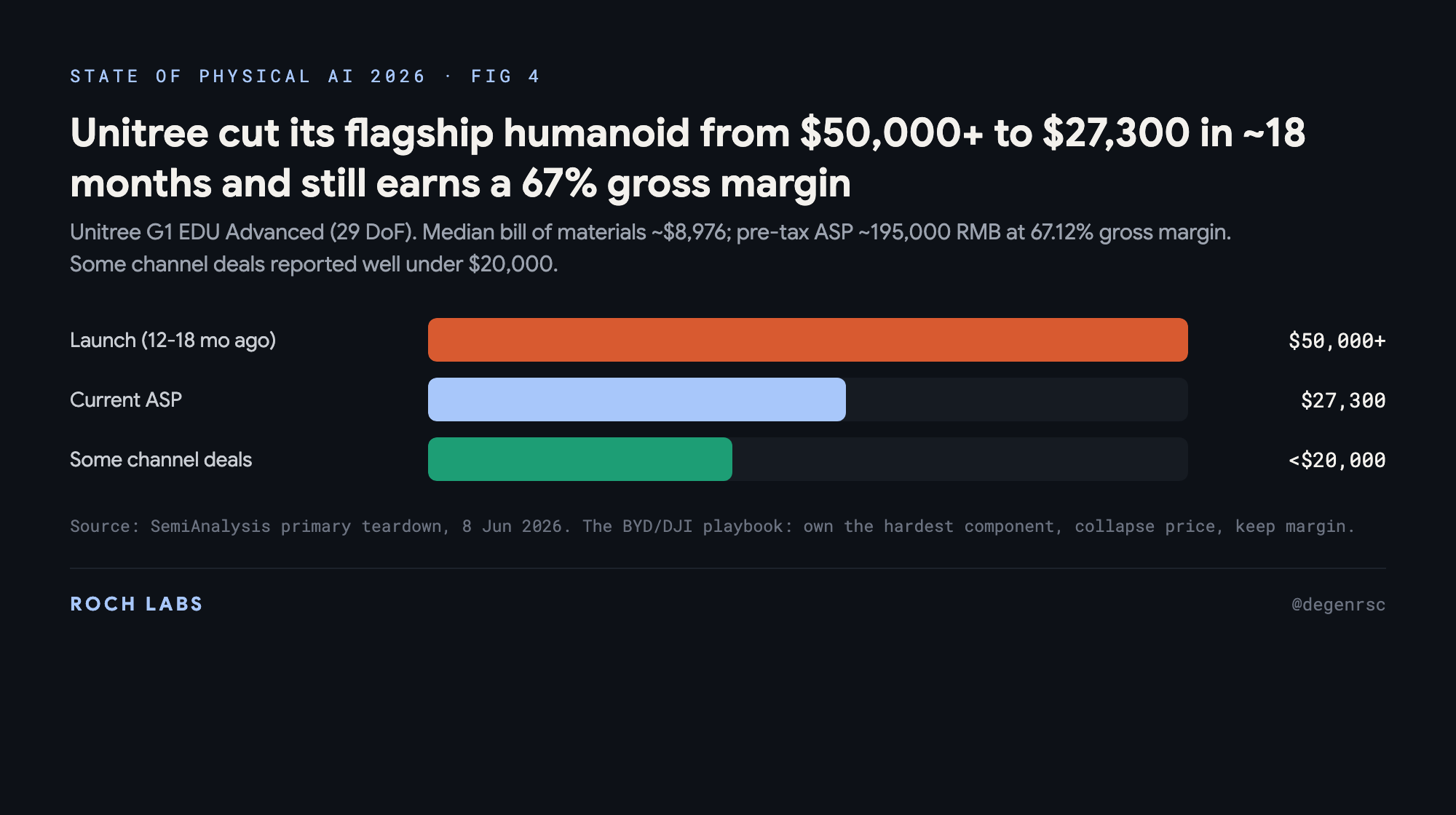

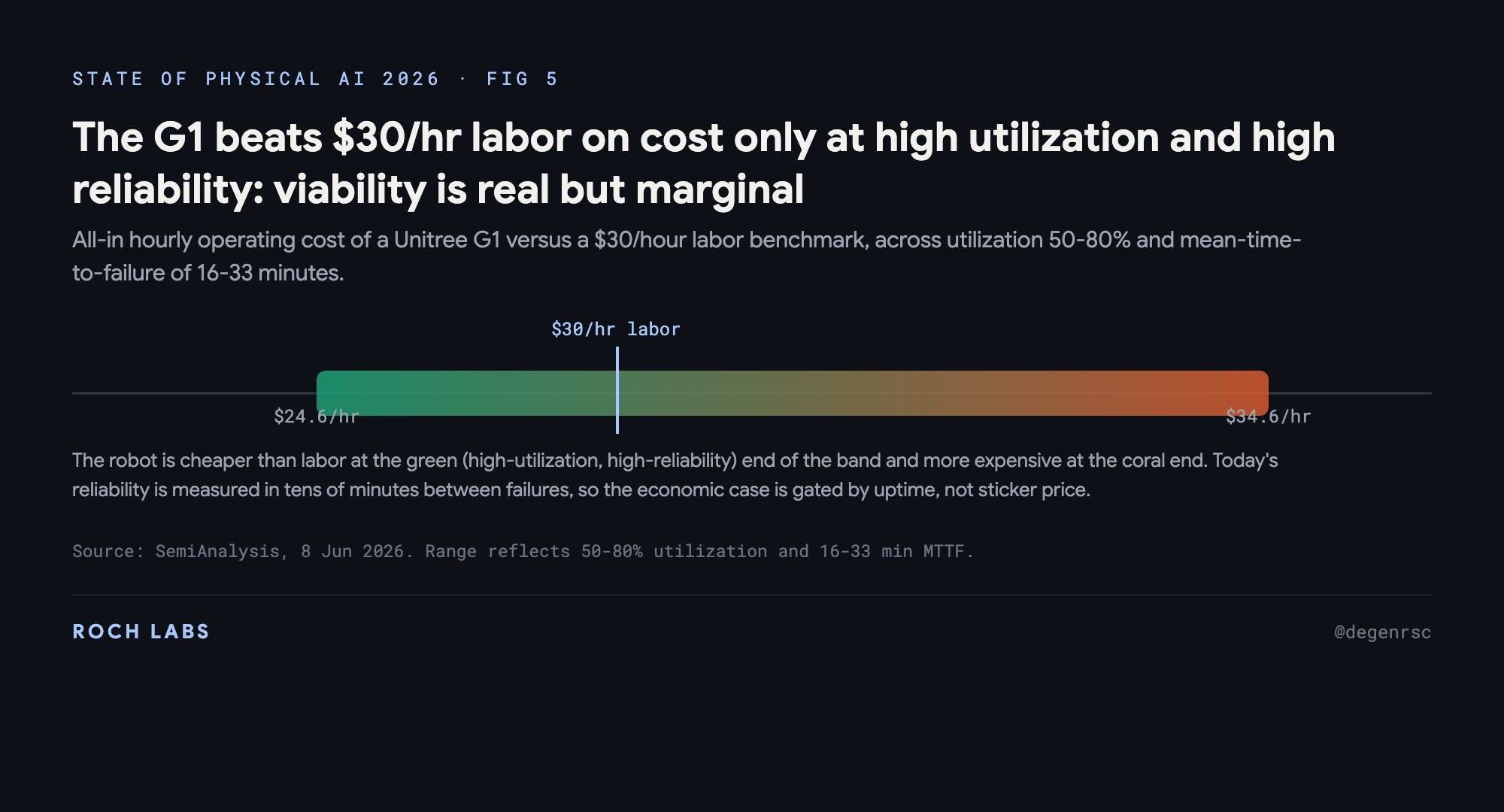

Here is the data point that should reset how you price the entire humanoid OEM basket. Per a SemiAnalysis primary teardown published in June 2026, the Unitree G1 EDU Advanced, a 29-degree-of-freedom humanoid, has a median bill of materials of approximately $8,976. Unitree’s pre-tax average selling price on that unit is roughly 195,000 RMB, which at the disclosed 67.12 percent gross margin is approximately $27,300. The same class of robot was priced above $50,000 twelve to eighteen months earlier. Unitree compressed the price of a working humanoid by roughly 45 percent and is still earning a 67 percent gross margin on it, with some channel deals reported “well under $20,000.”

Read that the way a hardware investor reads it. A company that can cut the price of its flagship nearly in half and keep a two-thirds gross margin is not in a price war it is losing. It is running a deliberate cost-down campaign from a position of structural advantage, and it is doing it while tripling revenue year-over-year on a roughly 60 percent blended gross margin, spending roughly $300 million on AI research, in-housing its manufacturing, and pulling roughly $610 million from a STAR Market listing to fund the next leg. This is the BYD playbook and the DJI playbook applied to humanoids: own the hardest component, in Unitree’s case the quasi-direct-drive actuator, compound a cost advantage that competitors cannot match because they are buying that component rather than making it, and then eat the market from the bottom by collapsing price faster than anyone’s margin can survive.

The implication for the Western humanoid OEM basket is direct. If the reference product in the category sells a working unit at $27,300 and is heading under $20,000 while keeping 67 percent margins, then every pre-revenue Western OEM whose model assumes a $50,000-plus ASP and a “we will get cost down later” cost curve is modeling a world that already does not exist. The price umbrella they are implicitly underwriting has already been removed by the company that controls the cost-defining component. That is what makes the basket exit liquidity: it is priced for a margin structure that the Chinese cost leader has already demonstrated it can compress at will.

The one honest caveat on the Unitree cost story sits in the operating economics, not the sticker. Per the same SemiAnalysis work, the all-in hourly cost of running a G1 against a $30-per-hour labor benchmark lands somewhere between $24.60 and $34.60 per hour depending on utilization between 50 and 80 percent and mean-time-to-failure between 16 and 33 minutes. In other words, the robot beats human labor on cost only at high utilization and high reliability, and today’s reliability is measured in tens of minutes between failures. The viability is real but marginal, and it is gated by uptime, not by sticker price.

So the cost attack is genuine and the deployment economics are still on a knife’s edge. Both things are true. The investing conclusion is that the value is leaking toward whoever owns the actuator and the reducer, and away from whoever assembles the robot, which sends us to the one name the bulls point to as the Western-accessible chokepoint.

IV. China owns the upstream, not just the factory: roughly 90 percent of refined rare earths and the NdFeB magnets every actuator needs

The cost attack in the previous section is not a one-product fluke, and the reason it is durable sits upstream of the factory, in the raw materials. Every electric actuator in a humanoid robot depends on a permanent magnet, and the highest-performance permanent magnets are neodymium-iron-boron (NdFeB) magnets built from rare earth elements. Per multiple supply-chain analyses, China controls roughly 90 percent of global refined rare earth output and an even larger share of finished NdFeB magnet production. The mining is somewhat more distributed, but the refining and the magnet-making, the two steps that actually matter, are concentrated in China to a degree that has no near-term substitute.

This is the structural floor under the entire China cost advantage. A Western OEM can in principle design a better robot, but the motor inside its actuators is built from magnets that are refined and, in most cases, manufactured in China. When Beijing tightened rare earth and magnet export licensing through 2025, the binding constraint on Western humanoid production was not engineering talent or capital, it was access to the magnets, and the lead times stretched. The same dynamic that gave China drones through DJI, solar through a 90 percent cost decline, and batteries through CATL is now present one layer deeper in the robot than the actuator: in the magnet itself.

The investing read is uncomfortable but clear. The bull case for the Western and Japanese actuation incumbents implicitly assumes they can scale production to meet the humanoid ramp. That assumption runs straight into a materials chokepoint that China controls. It is also why the actuation layer, despite being the highest-value 40 to 66 percent of the bill of materials, is the layer where Western suppliers are least able to defend share on cost: you cannot out-engineer a magnet you cannot source. This is the most underpriced structural risk in the entire Western physical AI basket, and it is why the cost collapse documented in the previous section compounds rather than mean-reverts.

V. The chokepoint that is supposed to win is margin-compressing while priced at triple-digit revenue multiples: LeaderDrive’s gross margin fell 5.62 points as the share war started

LeaderDrive, ticker 688017 on the Shanghai STAR Market, is the name that sits at the top of Goldman’s component hierarchy. It is the dominant Chinese harmonic-reducer maker, the single most defensible position in the entire physical AI value chain on paper, and it is the cleanest test of the chokepoint thesis. The test does not pass at today’s price.

The growth is real. Per company filings, LeaderDrive’s fiscal 2025 revenue was approximately 570 million RMB, up 47 percent year-over-year, and net profit was approximately 125 million RMB, up 122 percent. Those are excellent top-line numbers. The problem is the margin and the multiple. Per the H1 2025 disclosure, LeaderDrive’s gross margin was 34.77 percent, down 5.62 percentage points year-over-year. The single most defensible component in the chain saw its gross margin compress by more than five points in the same period that humanoid demand was supposedly inflecting, which tells you the reducer market is already a share war, not a pricing-power monopoly. China’s domestic harmonic-reducer share is already 30 to 40 percent per JPMorgan estimates, and LeaderDrive’s named customers, Agibot and UBTech, are Chinese OEMs, the same ecosystem running the cost-down.

Now the valuation. Revenue of approximately 570 million RMB is roughly $78 million. Against a market capitalization of roughly $8 to $11 billion, that is a triple-digit price-to-sales multiple on a business whose gross margin is contracting. You are being asked to pay over 100 times revenue for the privilege of owning the chokepoint precisely as the chokepoint demonstrates it has less pricing power than the map implies. The chokepoint thesis is correct in structure and wrong at this price. That distinction, right structure and wrong price, is the difference between a thesis and a trade.

One fact I want to handle precisely, because the bull case leans on it: LeaderDrive is widely reported as a Tesla Optimus harmonic-reducer supplier. The naming-confusion theory I held earlier does not survive scrutiny: “LeaderDrive” and “Suzhou Green Harmonic” are two English renderings of one Suzhou-based company, whose Chinese name translates literally as “Green Harmonic,” not two different suppliers. The names were the confusion, not evidence of a second vendor. So that is not the issue. The real issue is the strength of the claim. Per trade-media supply-chain reporting, Tesla completed factory audits for its third-generation Optimus with Chinese suppliers taking roughly 70 percent of component share, and LeaderDrive is named among the harmonic-reducer suppliers in that chain. But unlike Sanhua, which has a confirmed roughly $685 million Optimus-related order, there is no disclosed contract value or official qualification specific to LeaderDrive. So the honest characterization is probable supplier, not confirmed exclusive design-win, and certainly not disclosed economics. It does not change the verdict. Even granting the Tesla link, LeaderDrive is margin-compressing at a triple-digit multiple, so the structure is right and the price is wrong. A confirmed, sized Tesla contract is the catalyst that would force a re-rate, and it is the single most important thing to watch on this ticker.

The Japanese incumbent, Nabtesco, ticker 6268, scores at the top of Goldman’s reducer ranking alongside LeaderDrive and is the established precision-reducer supplier to global industrial robotics. It is the cleaner Western-accessible way to own the reducer chokepoint, and it is under the same Chinese price attack from below. Nabtesco is a watch-on-weakness name, not a buy here, for the same reason: the structural position is real and the pricing environment is deteriorating as Chinese reducers move up the quality curve.

VI. The capability ceiling is lower than the demos imply: robotics has its foundation-model moment but not its internet, and robots have almost none of the proprioception humans use

Set the economics aside and ask the harder question: can these machines actually do general work yet? The honest answer from the research frontier is no, and the reason is structural, not incremental.

Per a June 2026 survey paper on arXiv from a group including Schwager, Hutter, and Peters, the field has reached its “foundation-model moment” in the sense that large vision-language-action models can now be trained for robotics, but it has not reached its “internet moment,” meaning there is no web-scale corpus of grounded physical interaction data to train on. Language models had the entire internet. Robotics has a few thousand teleoperated demonstrations per task and no equivalent of the open web. The grounding layer, the mapping from a model’s abstract plan to reliable physical action in an unstructured environment, is unsolved. This is why the impressive demos are almost always in constrained settings and why mean-time-to-failure is still measured in tens of minutes.

Pair that software gap with a hardware one that gets even less attention: proprioception. Humans sense the world through an enormous distributed network of touch, force, and position receptors, and roughly 70 percent of human sensing is not vision. Today’s humanoids have almost none of that. They are running on cameras and a handful of joint encoders, which is why dexterous manipulation, the thing that would make a humanoid economically general, remains the hardest unsolved problem and why Goldman ranks the dexterous hand module second in its entire component hierarchy. The sensing layer is both underbuilt and undervalued.

The investing translation: the timeline to general-purpose, unsupervised, deployed-at-scale humanoid labor is longer than the basket’s valuations imply, and the binding constraints are a data corpus that does not exist yet and a sensing stack that has barely been built. That does not kill the sector. It means the sector pays off on a longer clock than the spot prices assume, which again favors patience and chokepoints over the hype basket.

VII. The on-chain robotics basket is almost entirely subsidy-masked or simulated revenue: of eleven tokens audited on-chain, only one shows real, verified, converging revenue

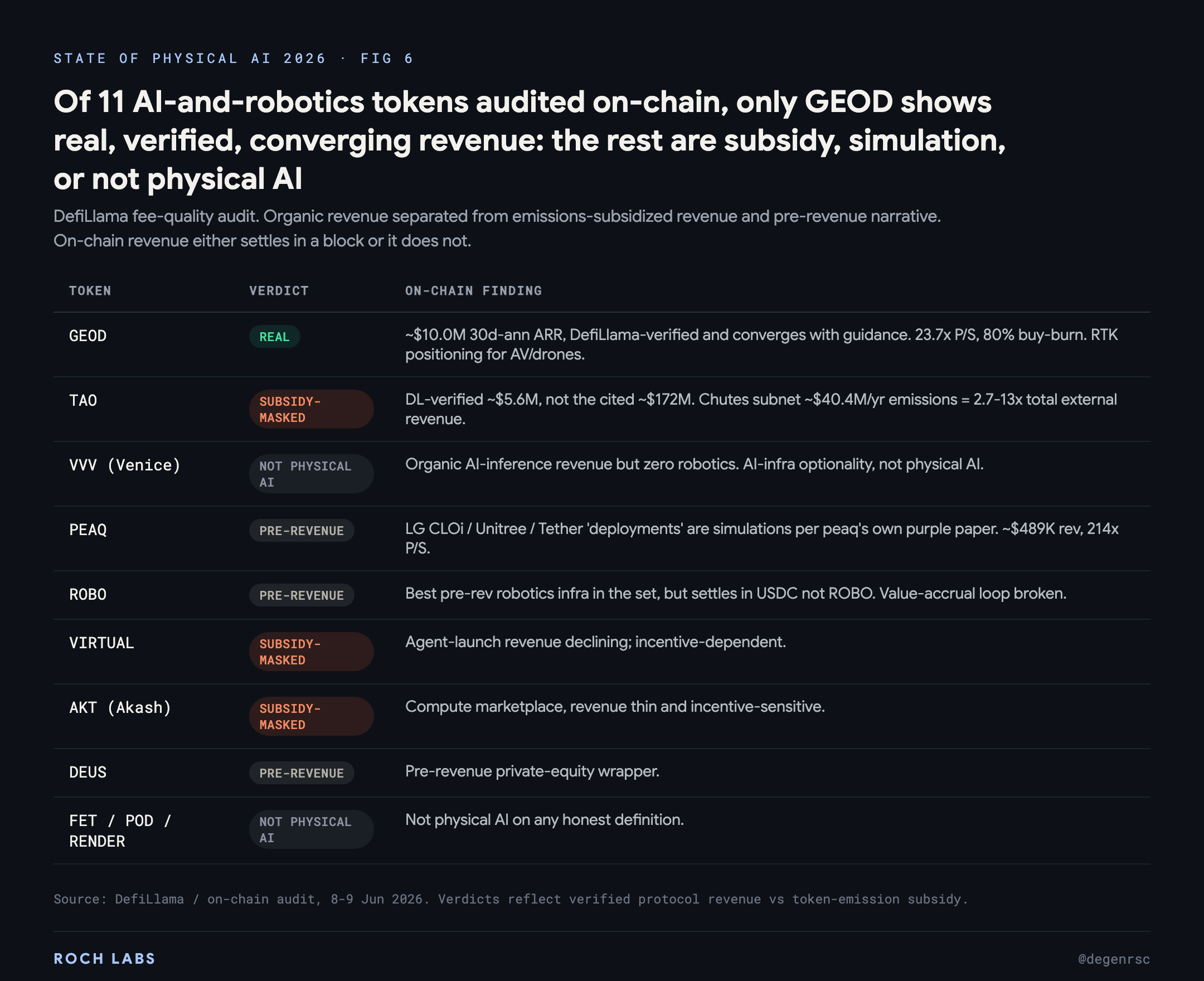

The crypto expression of physical AI is where the gap between narrative and substance is widest, and it is the part of this report I can verify most precisely, because on-chain revenue either settles in a block or it does not. I ran eleven AI-and-robotics tokens through a DefiLlama fee-quality audit, sorting organic revenue from subsidy-masked revenue from pre-revenue narrative. The result is stark: one token has real, verified, converging revenue. The rest are optionality, subsidy, or simulation.

GEOD, the Geodnet decentralized RTK-positioning network, is the lone survivor of the audit. Per DefiLlama, its trailing 30-day annualized revenue is approximately $10.0 million, and critically that on-chain figure converges with the company’s own guidance rather than contradicting it, which is the single best sign that revenue is real. It trades at roughly 23.7 times fully-diluted price-to-sales, runs an 80 percent buy-and-burn on protocol revenue, and sells a real product: high-precision positioning infrastructure for autonomous vehicles and drones, which is genuinely a physical AI input. The honest risk is a July 30 halving that cuts node rewards and could trigger node churn if the unit economics for operators tighten. But it is the one name where the on-chain data and the business agree.

TAO, the Bittensor token that anchors most “decentralized AI” portfolios, fails the audit in an instructive way. The widely-cited revenue figure of roughly $172 million is not real protocol revenue. DefiLlama-verified revenue is approximately $5.6 million, and the largest subnet, Chutes, was running approximately $40.4 million per year in emissions subsidy, which is 2.7 to 13 times the network’s total external revenue depending on how you count. That is not a business, it is an income desert with a token-emission sprinkler. PEAQ, marketed as the machine-economy chain, is pre-revenue: its showcase “deployments” with LG CLOi, Unitree, and Tether are, per peaq’s own purple paper, simulations, not live revenue-generating integrations, against approximately $489,000 of actual revenue at a 214 times price-to-sales multiple.

The rest sort cleanly into “not physical AI” or “infrastructure optionality.” VVV (Venice) has genuinely organic AI-inference revenue but zero robotics exposure, which makes it an AI-infrastructure name, not a physical AI one. VIRTUAL and AKT are subsidy-masked or revenue-declining. ROBO (the decentralized-robotics infra token) is the best pre-revenue infrastructure story in the set but settles its activity in USDC rather than its own token, which breaks the value-accrual loop. DEUS is a pre-revenue private-equity wrapper. FET, POD, and RENDER are not physical AI on any honest definition. The inductive read across all eleven: the token market has priced a robotics-revenue narrative onto a set of assets where, with one exception, the robotics revenue does not yet exist on-chain. GEOD is the only place the narrative and the ledger agree.

VIII. The deployers are where physical AI is already profitable, and the market is not looking: Amazon runs more than one million robots for $4 to $10 billion a year in savings

Everything to this point has been about who builds the robot and who captures the component margin. The most direct way to express physical AI, though, is not to own the builders at all. It is to own the operators who deploy robots at scale and watch their margins expand. This layer is already profitable, already disclosed in earnings, and almost entirely ignored by the humanoid narrative, which is staring at the demo and missing the deployment.

The anchor data point is Amazon. Per Morgan Stanley estimates, Amazon now operates more than one million robots across roughly 300 fulfillment facilities, generating a reported $4 billion to $10 billion per year in operating savings. That is not a 2030 projection or a pilot. It is recurring margin showing up in the cost line of the largest logistics operation on earth, built on wheeled and articulated automation rather than humanoids, which is precisely the point: the money in physical AI today is being made by deployers running un-glamorous, single-purpose machines at industrial scale, not by anyone selling a bipedal robot.

The pattern generalizes to a screenable thesis: own the operators with a deployed fleet, a proprietary operational dataset, and a locked distribution channel, where each incremental robot expands margin rather than burns capital. Intuitive Surgical is the cleanest listed example, which is why it leads my conviction map, but the same logic points at the warehouse and logistics operators (Amazon and the third-party logistics names), the quick-service-restaurant operators automating the back of house, and the grocery and fulfillment deployers. The honest caveat is that for most of these the robotics line is not yet separable in the financials, so you are buying the deployer for the whole business and treating robotics margin as embedded optionality rather than a clean pure-play. But it is the layer where physical AI is already cash-generative, and it is structurally insulated from the China cost war, because the deployer captures value from operating the robot, not from manufacturing it. The cheaper the robot gets, the better the deployer’s economics become. China collapsing the hardware price is a tailwind for this layer, not a threat.

IX. The trade: own the data-moats and the one real on-chain cash flow, watch the chokepoints for a real pullback, avoid the basket that is exit liquidity

Pull the threads together and the portfolio writes itself, and it looks nothing like the basket. The shipment floor is tiny and concentrated in China and low-spec units. The value-capture layer is mechanical and is being commoditized by the Chinese cost leader at a 67 percent margin. The Western-accessible chokepoint is margin-compressing at a triple-digit multiple. The capability ceiling is gated by a data corpus and a sensing stack that do not exist yet. And the on-chain basket is, on verified data, one real business wearing ten costumes. The conclusion is not “avoid physical AI.” It is “own the narrow, defensible, cash-generative or moat-protected set, and let the hype basket find its real clearing price without you.”

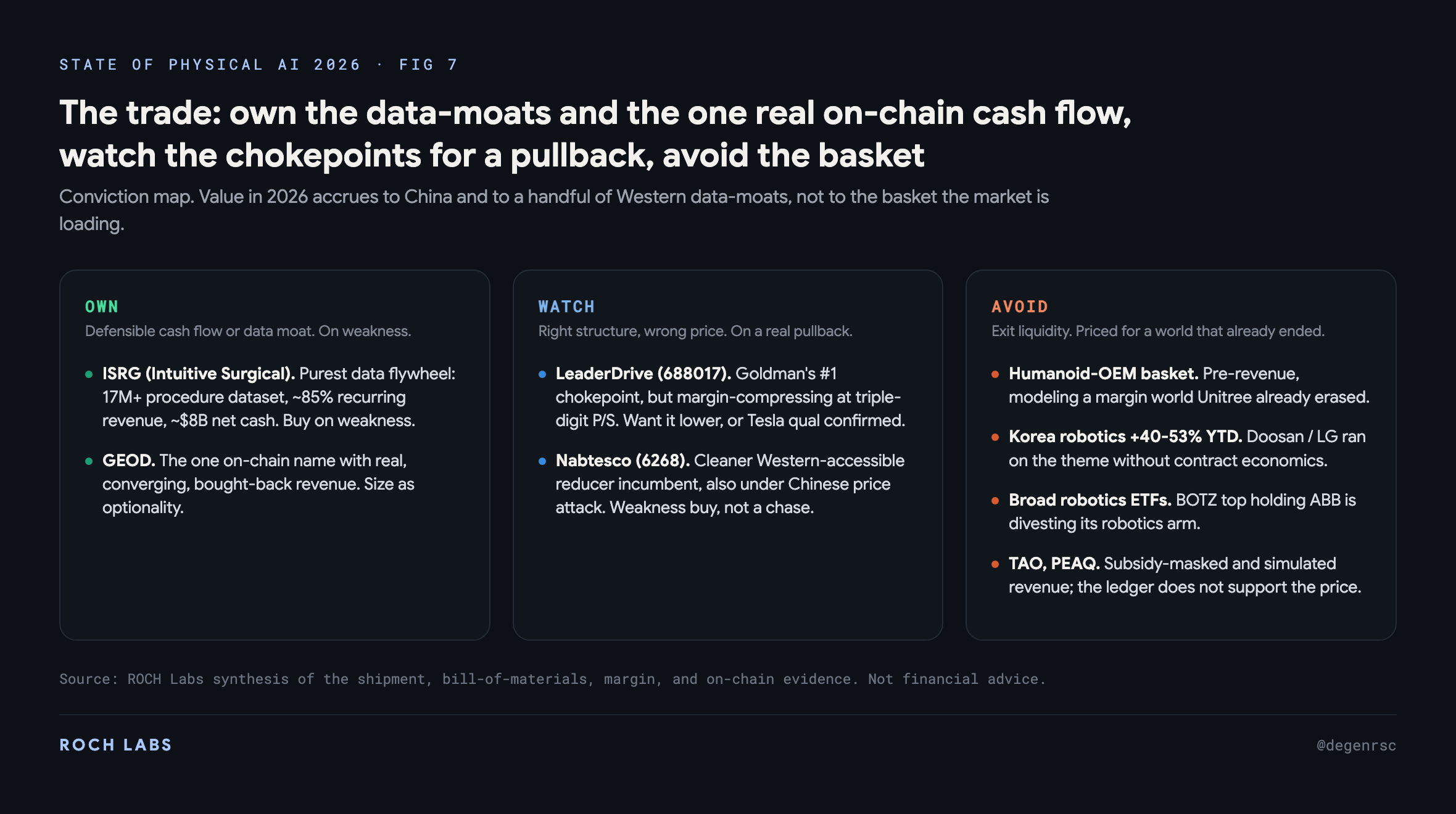

What I would own

Intuitive Surgical, ticker ISRG, is the purest data-flywheel in robotics that you can actually buy. It has a dataset of more than 17 million procedures, roughly 85 percent recurring revenue, and approximately $8 billion in net cash, and it sits outside the humanoid hype entirely, which is exactly why it is investable: you are buying a deployed fleet, a proprietary data moat, and a locked channel, not a target. My stance is buy on weakness rather than chase, because the quality is not in dispute and the entry is everything. On the on-chain side, GEOD is the only token I would hold on fundamentals rather than narrative, sized as optionality, because it is the one name where the revenue is real, converging, and bought back.

What I would watch and own only on a real pullback

LeaderDrive (688017) is the structurally correct chokepoint at a structurally wrong price; I want it materially lower, or I want the Tesla qualification confirmed, before the triple-digit multiple is defensible. Nabtesco (6268) is the cleaner Western-accessible reducer incumbent, also under price attack, also a weakness buy rather than a chase. These are the names where being right about the structure still loses money if you pay today’s price.

What I would avoid as exit liquidity

The pre-revenue Western and Chinese humanoid-OEM basket, which is modeling a margin world the Chinese cost leader has already erased. Korean robotics at plus 40 to 53 percent year-to-date, where names like Doosan and LG Electronics have run on the theme without the contract economics to support the move. Broad robotics ETFs, where the structure works against you: BOTZ’s top holding, ABB, is in the process of divesting its robotics division, so the index is overweight a company exiting the very thesis the index sells. And the subsidy-masked or simulated tokens, TAO and PEAQ chief among them, where the on-chain ledger does not support the narrative the price embeds.

X. One thesis gap called outright

One gap in this thesis is genuinely unresolved, and a second is a limitation I want to name even though I have given the layer a full section above.

The unresolved one is thermal management. High-density actuation in a human-sized envelope generates heat that has to go somewhere, and thermal dissipation is plausibly a gating constraint on continuous-duty humanoid labor. I do not have a clean, investable, pure-play name for it, and I am not going to invent one to round out the framework. It is an open research question in this thesis, and if the binding constraint on deployment turns out to be heat rather than dexterity or data, the names that solve it are not in my conviction map yet.

The limitation is the financial legibility of the deployer layer in Section VIII. The thesis that the operators capture physical AI margin is sound, and the Amazon data proves the savings are real and recurring. But for most of these names the robotics contribution is not separable in the financials, so the cleanest pure-play expressions are scarce, ISRG being the rare exception, and everything else requires buying the whole business and treating robotics margin as embedded optionality. I have named the layer and made the structural case for it. I have not solved the problem of isolating its value cleanly, and that is the honest state of it.

The forward view

The physical AI narrative will be right eventually, and that is exactly the trap. A thesis that is correct on a ten-year horizon and mispriced on a two-year one is how money is lost being early to something true. The shipment data, the bill-of-materials map, the Unitree price collapse, the LeaderDrive margin squeeze, and the on-chain audit all point the same way: in 2026 the volume and the margin in physical AI accrue to China and to a handful of Western data-moats, not to the basket the market is loading. The next twelve months will not be decided by who has the best humanoid demo. They will be decided by three things I will be tracking specifically: whether Unitree’s price keeps falling while margins hold, whether LeaderDrive confirms a Tesla design-win or sees its margin keep compressing, and whether the deployer layer starts showing the margin expansion that would make the whole thesis pay off in boring, ownable equities rather than pre-revenue hope.

Own the chokepoints and the data-moats on weakness. Let the basket find its clearing price without you.