The QCOM Setup: Why Edge Inference is the key, and what makes QCOM so special

A supply chain scoop, a $45B automotive pipeline, and 39 analyst desks still running a 2022 model.*

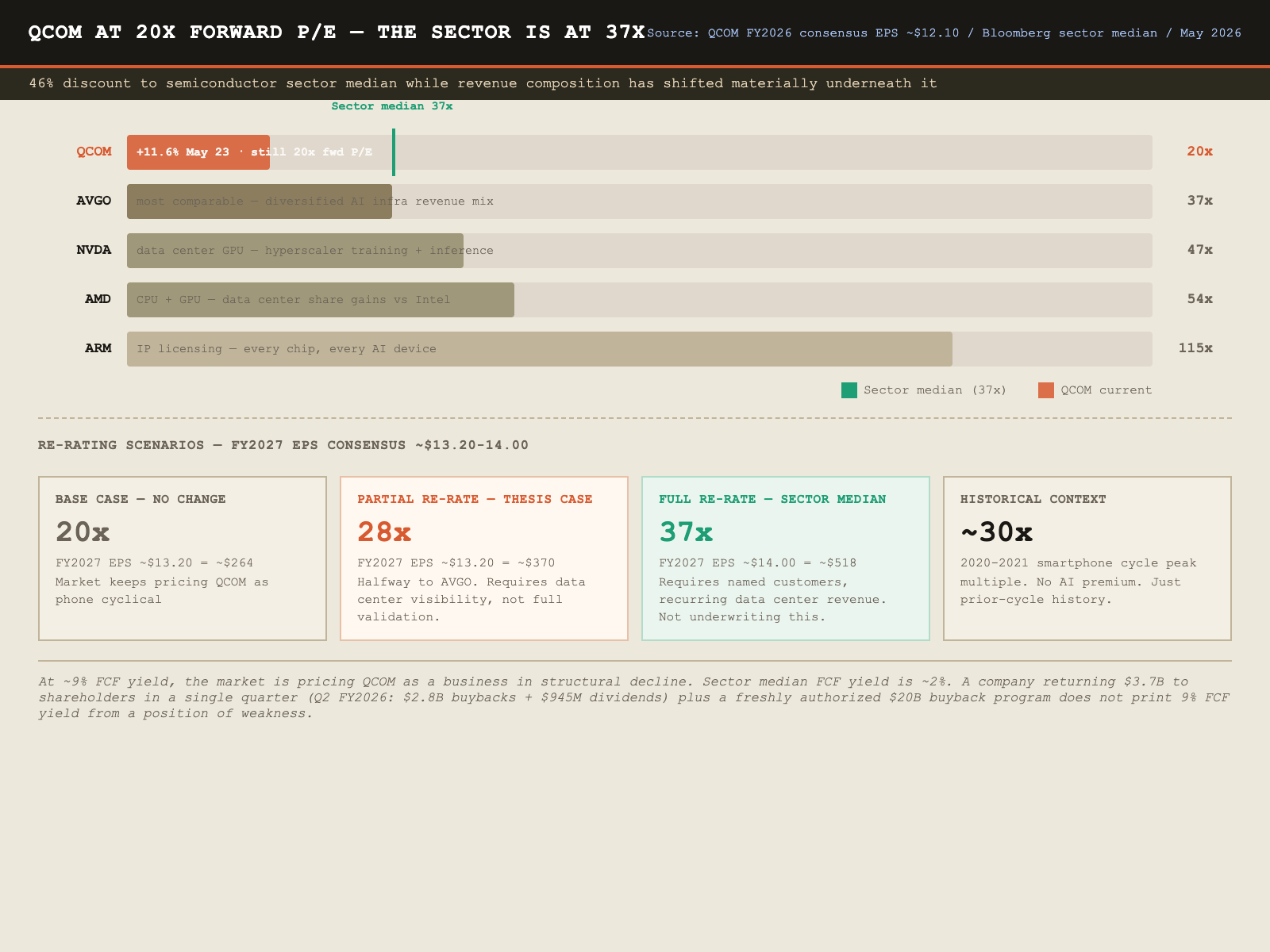

Qualcomm is priced as a smartphone chipmaker at a 46% discount to the semiconductor sector median. The revenue mix says it stopped being primarily a smartphone business a while ago. That gap between the label and the numbers is the trade.

Why I’m writing this now

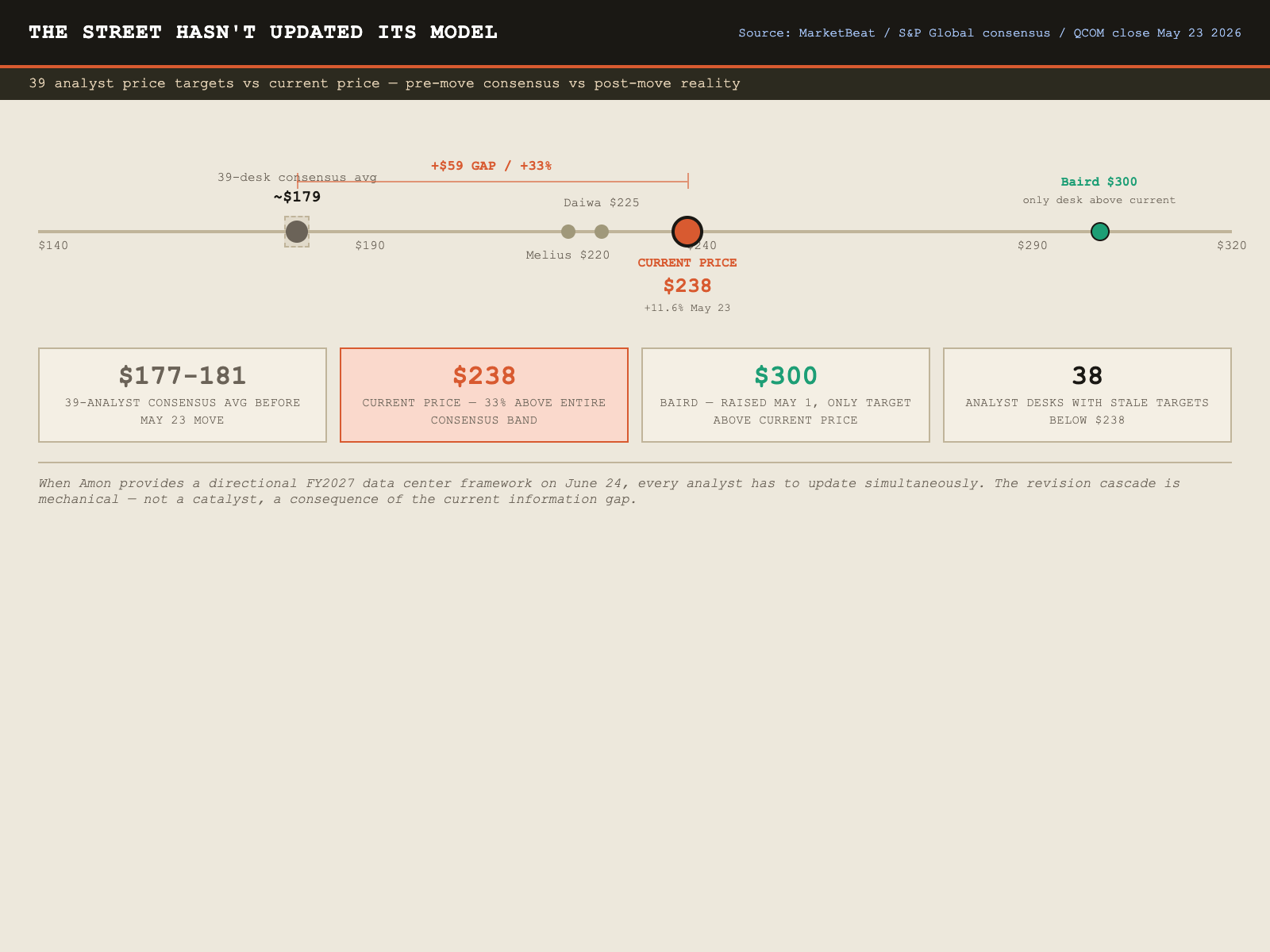

On May 23, 2026, QCOM moved +11.6% in a single session. Closed at $238.16. The 39-analyst consensus average target before that move was $177-$181. The stock blew clean through the entire analyst target band in one day.

Here’s the part that matters: none of those 39 desks have updated their models yet.

When Cristiano Amon provides any directional FY2027 framework at the June 24 Investor Day, every one of those analysts has to update simultaneously. That is not a catalyst. It is a mechanical consequence of where the price is relative to where the models are.

And then there’s the Ming-Chi Kuo report. Kuo (TF International Securities, 233K followers, the highest-credibility supply chain analyst in consumer electronics) published a survey in late April reporting that Qualcomm and MediaTek are co-development partners with OpenAI on a custom smartphone processor designed for an AI Agent-focused phone. 924K impressions. 179 quote-tweets. Mass production target 2028. Revenue per chip: Kuo estimates one AI chip project is worth 30-40 standard mobile processors in revenue. I’ll come back to what this means and what the limits of it are.

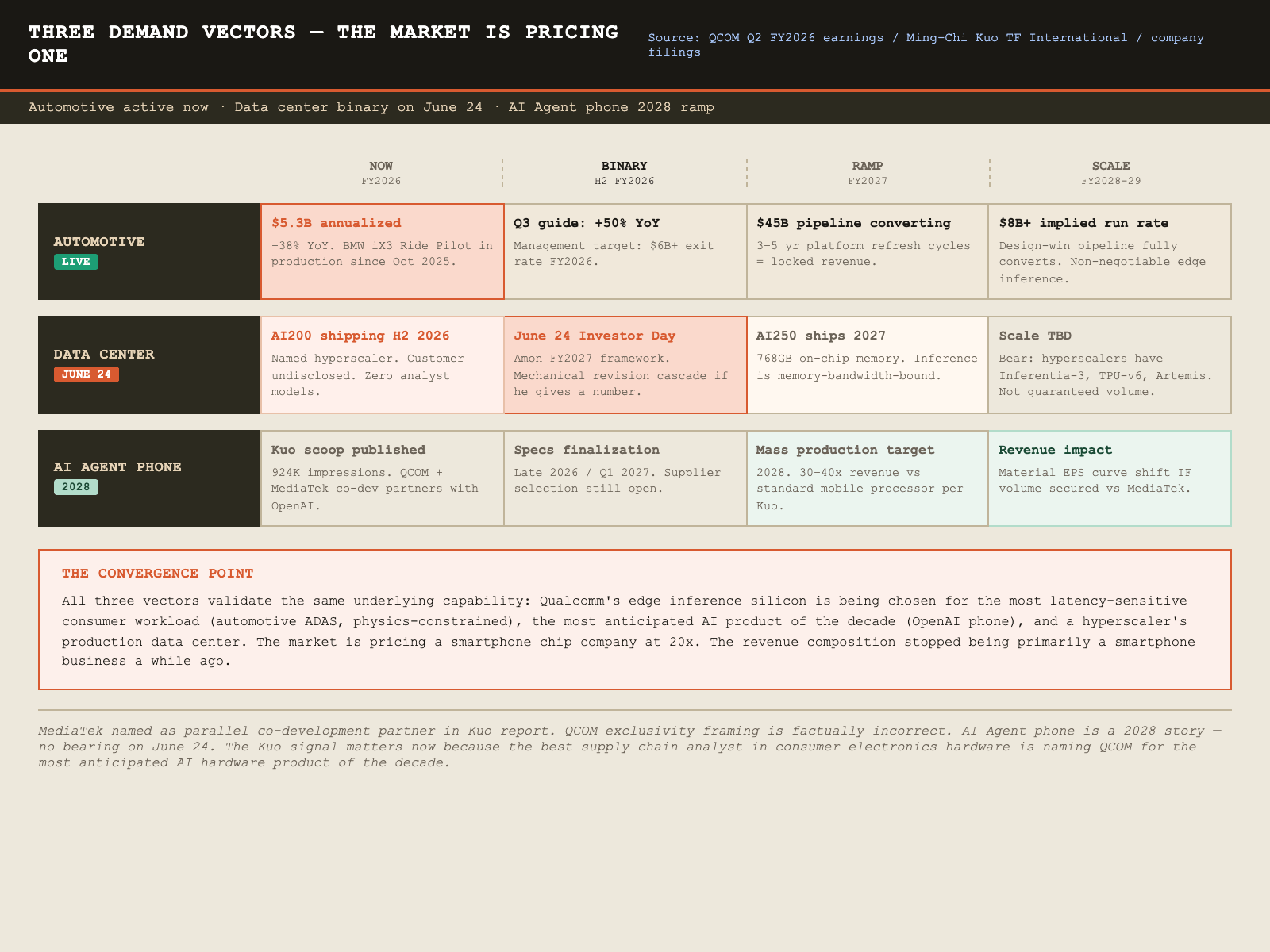

Three demand vectors are building simultaneously. The market is pricing one.

The three demand vectors

1. Automotive: the cleanest moat in the story

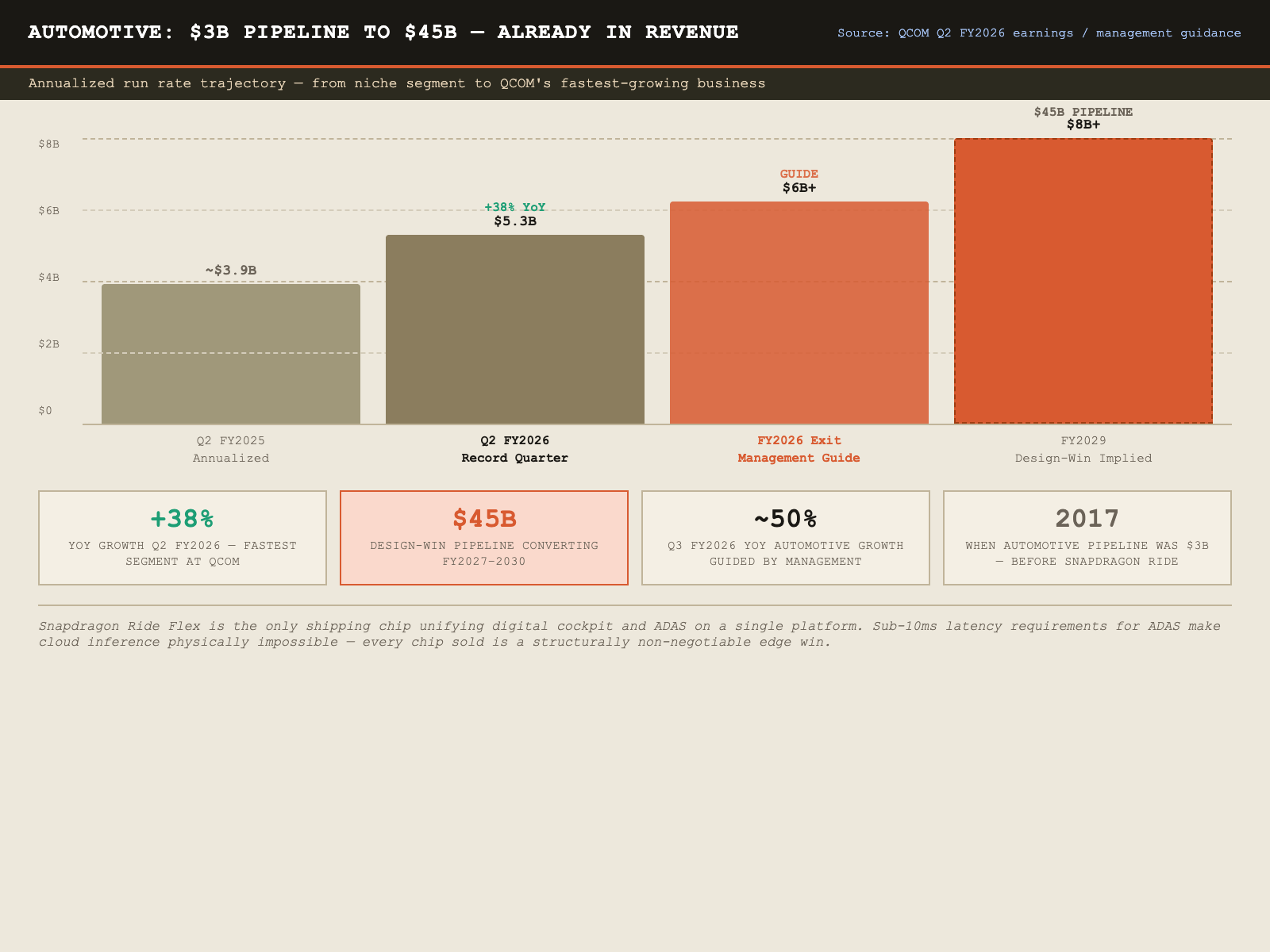

Automotive is a genuinely different business from mobile. ADAS inference cannot go to the cloud. Sub-10ms latency requirements for safety-critical workloads make cloud inference physically impossible. Not economically suboptimal. Physically impossible. The round-trip latency on any cloud connection is 40-80ms under ideal conditions. A collision avoidance model cannot wait 40ms. Every automotive ADAS chip sold is a permanent, structurally non-negotiable edge inference win.

The numbers, per Q2 FY2026 earnings and Q3 guidance:

Automotive revenue: $1.33B in Q2 (+38% YoY, record quarter)

Annualized run rate: crossed $5B for the first time

Q3 FY2026 guide: ~50% YoY automotive growth

FY2026 exit run rate target (management): >$6B annualized

Design-win pipeline: $45B (from $3B in 2017)

In production now: BMW iX3 Ride Pilot since October 2025

The $45B pipeline converts across FY2027-2030. This is not a “future promise” number. It is already in quarterly revenue, growing faster than any other segment, with 3-5 year platform refresh cycles baking in the next few years of revenue before the contracts even need renewing.

Snapdragon Ride Flex is the only shipping chip that unifies digital cockpit and ADAS on a single platform. NVIDIA Orin and Thor are high-performance AV, a different tier entirely. No direct competitor in the unified cockpit+ADAS space.

This is the demand vector the market is most under-pricing because it doesn’t look like “AI” in the way NVDA’s data center revenue looks like AI. It is. It just runs at 90mph on a highway in Munich instead of in a hyperscaler rack.

2. Data center: the binary on June 24

Amon confirmed on the Q2 FY2026 earnings call that Qualcomm will ship custom data center processors to a named hyperscaler before end of 2026. The customer has not been disclosed. The AI200 targets commercial shipments in 2026. The AI250 ships in 2027 and carries up to 768GB onboard memory, which matters because inference at scale is memory-bandwidth-bound, not compute-bound.

Here is the critical point: as of May 2026, there are zero FY2027 revenue estimates for AI200/AI250 on any bank desk. Zero. Not a single analyst has published a quantified FY2027 data center contribution. There is nothing to model yet because Amon has not given a number. When he gives even a directional range on June 24, every analyst is forced to build a model from scratch for a business line currently sitting at zero in their spreadsheet.

The stock was at $238 with every desk at $177. Whatever the June 24 number implies, the revision cascade follows mechanically regardless of whether the fundamental thesis is right.

The bear argument here deserves fair treatment: Google TPU-v6, Amazon Inferentia-3, and Meta Artemis all already exist. Hyperscalers have structural incentives to keep inference in-house and the capability to do it. The unnamed hyperscaler shipment could be a 5,000-unit evaluation run that never converts to commercial volume. One cancelled NRE agreement wipes the narrative. If Amon delivers no FY2027 framework on June 24, the data center thesis stays speculative and the multiple ceiling reverts to 20-22x on handset/auto fundamentals alone.

3. AI Agent phone: a 2028 story, not a 2026 trade

The Kuo report is worth understanding precisely because it is being misread in both directions.

What it says: Qualcomm and MediaTek are co-development partners with OpenAI on a custom smartphone processor for an AI Agent phone. The chip handles on-device context awareness and small-model inference continuously. Heavy compute offloads to cloud. Mass production target 2028. Specs and supplier selection expected finalized late 2026 or Q1 2027.

What it does not say: that QCOM is exclusive. MediaTek is named in the same sentence. Anyone running a thesis that relies on QCOM being the only partner here is building on a factually incorrect premise.

The revenue math is why this landed with 924K impressions: Kuo frames one AI chip design win as equivalent to 30-40 standard mobile processors in revenue potential. If that holds and QCOM secures meaningful volume for the 2028 ramp, the EPS curve changes materially. At current QCOM automotive ASP dynamics as a reference, that is not an unreasonable order-of-magnitude estimate.

This is a 2028 story. It has no bearing on June 24. The reason it matters now is signal quality: the best supply chain analyst in consumer electronics hardware is naming QCOM as a co-development partner on the most anticipated AI hardware product of the decade. That does not happen to a company the market should be pricing as a smartphone cyclical at 20x.

The CT indicator is also worth noting. Jukan05 (124K followers, tech equity account, was explicitly bearish on QCOM as recently as January 2026) quote-tweeted the Kuo report with: “Should I put together a bull thesis on Qualcomm? $QCOM.” 60 replies. 363 bookmarks on a single question post. He has not published the full thesis yet. When he does, it will circulate widely. Narrative formation at 124K follower accounts with 363 bookmarks per post is a leading indicator of broader CT uptake.

The valuation math

At $238, QCOM’s forward P/E is approximately 20x against FY2026 consensus EPS of ~$12.10. The semiconductor sector median forward P/E is 37x. That is a 46% discount.

For comparison:

NVDA: ~47x forward P/E

AMD: ~54x

ARM: ~115x

AVGO (most comparable on diversified AI infrastructure revenue mix): ~37x

The FCF yield case is the other side of this. At ~9% FCF yield, the market is pricing QCOM the way you price a business in structural decline. The sector median FCF yield is ~2%. A company returning $3.7B to shareholders in a single quarter (Q2 FY2026: $2.8B buybacks + $945M dividends) plus a freshly authorized $20B buyback program does not print 9% FCF yield from a position of weakness.

The historical context matters here. QCOM traded at ~30x P/E during the 2020-2021 smartphone cycle peak. No AI premium required. Just re-rating the automotive and IoT mix shift to something closer to prior-cycle highs would imply $260-280 on EPS alone. The stock is not expensive relative to its own history. It is trading near mid-cycle valuation while the revenue composition has shifted materially underneath it.

Re-rating to the sector median (37x) on FY2027 EPS of ~$14.00 implies ~$518. I am not underwriting that. It requires a fully validated data center business with named customers and recurring revenue, which does not exist yet.

The scenario I think is underwritten:

Partial re-rating to 28x (halfway between current 20x and AVGO’s 37x) on FY2027 EPS of ~$13.20 implies ~$370, approximately +55% from $238. This does not require QCOM to become NVDA. It requires the Street to stop pricing it as a phone chip company once data center revenue becomes visible.

The honest bear case

The arithmetic runs first.

QTL generated $1.38B in Q2 FY2026 at 72% EBT margin. That is approximately $1B per quarter in high-margin profit, representing ~30% of non-GAAP operating income. The Apple licence is terminable. If it expires unrenewed, nothing in automotive or IoT replaces that margin on a two-year timeline. This risk sits entirely outside the edge inference and data center thesis and does not get better if both theses deliver.

Against the edge inference case: AI Hub has 1,800 registered companies and 175+ pre-optimized models. It also has zero published DAU, MAU, or deployment volume figures anywhere. “1,800 companies” is a registration count, not an active usage figure. The platform is real. The adoption depth is unverifiable from public data. MediaTek’s Dimensity 9500 demonstrated a 20B-parameter LLM running on-device. The premium positioning QCOM relies on in Android is compressing faster than the bull case assumes. Thermal throttling is also real: sustained on-device inference degrades significantly from burst-mode TOPS claims under thermal limits. QCOM’s marketing figures are burst-mode. The sustained benchmark that matters more as usage patterns evolve is lower.

Against the data center bet: the specific architecture of the AI Agent phone (small model on-device, heavy compute offloads to cloud) means QCOM is not a play on AI data center scale. The OpenAI phone validates edge inference, not cloud inference. The AI200/AI250 is a separate product line from a different category. One validates the thesis that QCOM knows how to build inference silicon. The other has to stand on its own commercial merits, which are unproven.

The historical reversion pattern is worth naming explicitly. QCOM has run a diversification re-rating story four times: RF front-end (2019), IoT (2021), automotive (2023), and now AI/data center (2026). Each prior attempt saw the multiple expand and then contract when a handset guidance cycle disappointed. The automotive revenue evidence in the current cycle is stronger than in any of the prior three attempts. But the pattern exists and Q3 FY2026 handset guidance -- management guided ~$4.9B in handsets for Q3, down from $6B in Q2 -- means the near-term handset print could reassert the cyclical narrative if it misses.

The trade

I am not positioned yet. This is a pre-event setup note.

Entry: $199-207. The post-earnings support base from May 15-21 (five consecutive daily closes), the June-July 2024 structural zone, and approximately 20x forward P/E on FY2026 consensus all converge in that range.

Stop: $189 daily close. Below the May 20 swing low of $191.02. Risk at entry: 6-9%.

TP1: $247.9. Reclaim of May 12 intraday high. Pure mechanics, no thesis confirmation required.

TP2: $300. No overhead supply on weekly chart between $248 and $300.

TP3: $350-370. Full thesis, conditional on June 24 delivering a quantified FY2027 data center framework.

R/R to TP1 from mid-entry (~$203): approximately 2.5:1. Catalyst window: June 24 Investor Day.

Where I land

One thing the Kuo report changes is the narrative ceiling. Before it, the QCOM re-rating case was a valuation argument against a still-skeptical market. After it, the highest-credibility supply chain analyst in the world is naming QCOM as a co-development partner on an OpenAI AI Agent phone with 30-40x the revenue potential of a standard mobile processor.

MediaTek is in the room too. The exclusive framing is wrong and I want to be precise about that.

But here is the thing about the setup as a whole. Automotive ADAS cannot go to the cloud on physics grounds. OpenAI is designing a phone around on-device inference. The unnamed hyperscaler is receiving custom data center processors before year end. These three demand vectors are not coincidental. They are converging on the same underlying capability: Qualcomm’s edge inference silicon is good enough to be chosen for the most latency-sensitive workload in consumer electronics (automotive), the most anticipated AI product of the decade (OpenAI phone), and a hyperscaler’s production data center.

The market is pricing a smartphone chip company at 20x.

The upgrade cascade is not a question of whether. It is a question of when. June 24 is the most likely trigger.

Watching closely.

*Conviction: MEDIUM. Not positioned. Upgrades to HIGH on two conditions: Amon delivers a quantified FY2027 data center framework on June 24, and Q3 automotive holds the guided ~50% YoY growth. One without the other is not a full re-rating.*

*Not investment advice.*

Sources

1. [QCOM Q2 FY2026 Earnings Press Release — Qualcomm Investor Relations](https://investor.qualcomm.com/news-releases/news-release-details/qualcomm-announces-second-fiscal-quarter-2026-results) — Q2 FY2026 automotive revenue $1.33B, +38% YoY; annualized run rate; $45B design-win pipeline; $2.8B buybacks + $945M dividends; $20B buyback authorization.

2. [QCOM Q2 FY2026 Earnings Call Transcript — Seeking Alpha](https://seekingalpha.com/article/4786000-qualcomm-qcom-q2-2026-earnings-call-transcript) — Cristiano Amon confirms custom data center processor shipment to named hyperscaler before end of 2026; AI200 commercial shipment timeline; Q3 FY2026 guidance including ~50% YoY automotive growth and ~$4.9B handset segment.

3. [Qualcomm Investor Day 2026 — June 24 — Qualcomm Investor Relations](https://investor.qualcomm.com/events-presentations) — Scheduled June 24, 2026. Amon to provide strategic framework; data center business update expected.

4. [Ming-Chi Kuo X Post — OpenAI AI Agent Phone: Qualcomm and MediaTek as Co-Development Partners](

— TF International Securities supply chain survey. QCOM and MediaTek co-development partners for OpenAI custom smartphone processor. Mass production target 2028. Revenue per AI chip estimated at 30-40x standard mobile processor. 924,241 impressions.

5. [Jukan05 X Post — QCOM Bull Thesis Framing](

— Quote-tweet of Kuo report. 124K follower tech equity account previously bearish on QCOM as of Jan 2026 flags intent to build bull thesis. 363 bookmarks.

6. [Snapdragon Ride Flex — Qualcomm Product Page](https://www.qualcomm.com/products/automotive/snapdragon-ride) — Unified digital cockpit and ADAS on single platform. Only shipping chip in this category. BMW iX3 Ride Pilot launched October 2025.

7. [MarketBeat QCOM Analyst Price Targets — Consensus Data](https://www.marketbeat.com/stocks/NASDAQ/QCOM/price-target/) — 39-analyst consensus average price target $177-$181 pre-May 23 move. Baird $300 target raised May 1, 2026. 38 desks below current price $238.

8. [S&P Global Market Intelligence — Semiconductor Sector Forward P/E Consensus](https://www.spglobal.com/marketintelligence/en/) — Semiconductor sector median forward P/E approximately 37x; NVDA ~47x; AMD ~54x; ARM ~115x; AVGO ~37x as of May 2026.

9. [QCOM Form 10-Q Q2 FY2026 — SEC EDGAR](https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=QCOM&type=10-Q) — QTL segment Q2 FY2026 revenue $1.38B at 72% EBT margin. Full financial statements.

10. [Qualcomm AI Hub — Developer Platform](https://aihub.qualcomm.com/) — 1,800+ registered companies, 175+ pre-optimized models as of May 2026. On-device AI model deployment platform.

11. [QCOM Historical Price Data — May 23, 2026 Session](https://finance.yahoo.com/quote/QCOM/history/) — Closing price $238.16, single-session move +11.6%. May 20 swing low $191.02.

12. [MediaTek Dimensity 9500 — On-Device LLM Benchmark](https://www.mediatek.com/products/smartphones/dimensity-9500) — 20B-parameter LLM on-device capability. Direct competition for premium Android AI processing against Snapdragon Elite.

13. [Qualcomm AI200/AI250 Data Center Processor Announcement](https://www.qualcomm.com/news/releases/2025/10/qualcomm-announces-ai-inference-processors-for-data-centers) — AI200 commercial shipments targeted 2026; AI250 ships 2027, up to 768GB onboard memory.